By Sunday night, when Mitch Mc, Connell forced a vote on a brand-new bill, the bailout figure had broadened to more than five hundred billion dollars, with this huge sum being assigned to two different propositions. Under the first one, the Treasury Department, under Secretary Steven Mnuchin, would supposedly be given a budget of seventy-five billion dollars to offer loans to particular business and markets. The second program would run through the Fed. The Treasury Department would supply the reserve bank with 4 hundred and twenty-five billion dollars in capital, and the Fed would use this cash as the basis of a mammoth financing program for companies of all sizes and shapes.

Information of how these plans would work are vague. Democrats stated the new costs would give Mnuchin and the Fed overall discretion about how the cash would be distributed, with little openness or oversight. They slammed the proposal as a "slush fund," which Mnuchin and Donald Trump could utilize to bail out favored business. News outlets reported that the federal government wouldn't even need to determine the aid recipients for approximately six months. On Monday, Mnuchin pressed back, stating people had actually misinterpreted how the Treasury-Fed partnership would work. He might have a point, but even in parts of the Fed there may not be much interest for his proposal.

during 2008 and 2009, the Fed faced a great deal of criticism. Evaluating by their actions so far in this crisis, the Fed chairman, Jerome Powell, and his coworkers would choose to concentrate on stabilizing the credit markets by acquiring and underwriting baskets of financial properties, instead of providing to specific business. Unless we are ready to let troubled corporations collapse, which could emphasize the coming downturn, we need a method to support them in a sensible and transparent manner that minimizes the scope for political cronyism. Fortunately, history provides a design template for how to conduct corporate bailouts in times of acute stress.

At the beginning of 1932, Herbert Hoover's Administration set up the Restoration Financing Corporation, which is frequently described by the initials R.F.C., to offer support to stricken banks and railways. A year later, the Administration of the recently elected Franklin Delano Roosevelt considerably broadened the R.F.C.'s scope. For the rest of the nineteen-thirties and throughout the Second World War, the organization supplied important financing for services, agricultural interests, public-works schemes, and catastrophe relief. "I believe it was a fantastic successone that is frequently misinterpreted or overlooked," James S. Olson, a historian at Sam Houston State University, in Huntsville, Texas, told me.

It slowed down the mindless liquidation of properties that was going on and which we see some of today."There were 4 secrets to the R.F.C.'s success: self-reliance, utilize, management, and equity. Established as a quasi-independent federal firm, it was overseen by a board of directors that included the Treasury Secretary, the chairman of the Fed, the Farm Loan Commissioner, and 4 other people selected by the President. "Under Hoover, the majority were Republicans, and under Roosevelt the bulk were Democrats," Olson, who is the author of a detailed history of the Reconstruction Finance Corporation, stated. "However, even then, you still had individuals of opposite political affiliations who were required to interact and coperate every day."The fact that the R.F.C.

Congress originally endowed it with a capital base of five hundred million dollars that it was empowered to take advantage of, or multiply, by issuing bonds and other securities of its own. If we set up a Coronavirus Finance Corporation, it could do the same thing without directly involving the Fed, although the main bank might well end up buying some of its bonds. At first, the R.F.C. didn't openly announce which organizations it was lending to, which resulted in charges of cronyism. In the summer of 1932, more transparency was presented, and when F.D.R. went into the White Home he discovered a skilled and public-minded person to run the company: Jesse H. While the initial goal of the RFC was to help banks, railways were helped since numerous banks owned railroad bonds, which had declined in value, since the railways themselves had suffered from a decrease in their service. If railroads recuperated, their bonds would increase in worth. This increase, or appreciation, of bond prices would enhance the financial condition of banks holding these bonds. Through legislation approved on July 21, 1932, the RFC was authorized to make loans for self-liquidating public works task, and to states to supply relief and work relief to needy and jobless individuals. This legislation also needed that the RFC report to Congress, on a monthly basis, the identity of all brand-new debtors of RFC funds.

Throughout the very first months following the facility of the RFC, bank failures and currency holdings beyond banks both decreased. Nevertheless, a number of loans excited political and public controversy, which was the reason the July 21, 1932 legislation consisted of the arrangement that the identity of banks getting RFC loans from this date forward be reported to Congress. The Speaker of the House of Representatives, John Nance Garner, bought that the identity of the borrowing banks be made public. The publication of the identity of banks receiving RFC loans, which began in August 1932, decreased the effectiveness of RFC financing. Bankers became unwilling to borrow from the RFC, fearing that public revelation of a RFC loan would trigger depositors to fear the bank remained in danger of stopping working, and possibly begin a panic (What is a consumer finance account).

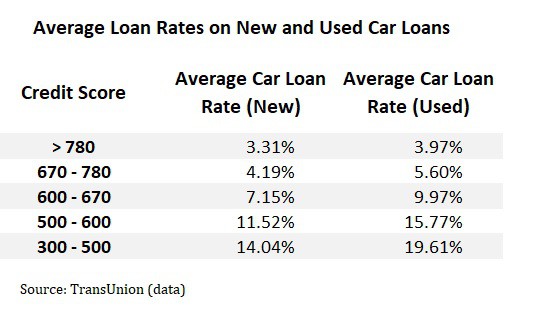

Some Known Questions About How To Finance A Private Car Sale.

In mid-February 1933, banking difficulties established in Detroit, Michigan. The RFC was prepared to make a loan to the distressed bank, the Union Guardian Trust, to avoid a crisis. The bank was one of Henry Ford's banks, and Ford had deposits of $7 million in this specific bank. Michigan Senator James Couzens required that Henry Ford subordinate his deposits in the distressed bank as a condition of the loan. If Ford concurred, he would run the risk of losing all of his deposits prior to any other depositor lost a cent. Ford and Couzens had once been partners in the vehicle service, but had actually ended up being bitter competitors.

When the negotiations stopped working, the governor of Michigan stated a statewide bank vacation. In spite of the RFC's determination to assist the Union Guardian Trust, the crisis might not be prevented. The crisis in Michigan resulted in a spread of panic, initially to nearby states, however eventually throughout the country. By the day of Roosevelt's inauguration, March 4, all states had actually stated bank holidays or had limited the withdrawal of bank deposits for money. As one of his very first function as president, on March 5 President Roosevelt announced to the country that he was declaring a nationwide bank vacation. Practically all banks in the country were closed for business throughout the following week.

The effectiveness of RFC providing to March 1933 was limited in several aspects. The RFC needed banks to promise assets as security for RFC loans. A criticism of the RFC was that it often took a bank's finest loan possessions as collateral. Therefore, the liquidity provided came at a steep cost to banks. Likewise, the promotion of brand-new loan receivers beginning in August 1932, and general controversy surrounding RFC lending most likely discouraged banks from borrowing. In September and November 1932, the quantity of outstanding RFC loans to banks and trust business decreased, as payments surpassed new loaning. President Roosevelt inherited the RFC.

The RFC was an executive agency with the ability to obtain financing through the Treasury exterior of the normal legal procedure. Thus, the RFC could be used to finance a variety of favored projects and programs without acquiring legal approval. RFC loaning did not count toward financial expenses, so the expansion of the function and impact of the government through the RFC was not shown in the federal budget. The first job was to support the banking system. On March 9, 1933, the Emergency Situation Banking Act was approved as law. This legislation and a subsequent amendment improved the RFC's capability to help banks by giving it the authority to acquire bank preferred stock, capital notes and debentures (bonds), and to make loans using bank favored stock as collateral.

This arrangement of capital funds to banks reinforced the monetary position of lots of banks. Banks might utilize the new capital funds to expand their financing, and did not have to pledge their best possessions as collateral. The RFC purchased $782 countless bank chosen stock from 4,202 private banks, and $343 countless capital notes and debentures from 2,910 individual bank and trust companies. In sum, the RFC helped almost 6,800 banks. Many of these purchases happened in the years 1933 through 1935. The favored stock purchase program did have controversial elements. The RFC authorities at times exercised their authority as shareholders to decrease incomes of senior bank officers, and on occasion, insisted upon a change of bank management.

In the years following 1933, bank failures decreased to extremely low levels. Throughout the New Deal years, the RFC's assistance to farmers was second only to its assistance to lenders. Overall RFC financing to agricultural financing institutions amounted to $2. 5 billion. Over half, $1. 6 billion, went to its subsidiary, the Product Credit Corporation. The Commodity Credit Corporation was integrated in Delaware in 1933, and operated by the RFC for 6 years. In 1939, control of the Product Credit Corporation was transferred to the Department of Agriculture, were it remains today. The farming sector was hit especially hard by anxiety, drought, and the intro of the tractor, displacing many small and occupant farmers.

Its goal was to reverse the decline of item prices and farm incomes experienced considering that 1920. The Commodity Credit Corporation contributed to this goal by acquiring picked agricultural products at guaranteed costs, normally above the dominating market value. Therefore, the CCC purchases established a guaranteed minimum cost for these farm products. The RFC likewise moneyed the Electric Home and Farm Authority, a program developed to make it possible for low- and moderate- earnings households to buy gas and electric home appliances. This program would create demand for electricity in rural areas, such as the location served by the brand-new Tennessee Valley Authority. Offering electrical energy to backwoods was the objective of the Rural Electrification Program.